The Lion, The Ayatollah, And The Oil Barrel

Will the Israel-Iran conflict make oil prices more expensive, and what are Iran's next moves?

In the early morning of June 13th, the Israeli Defence Forces (IDF) launched waves of airstrikes across roughly a hundred targets in Iran. Mossad, Israel’s spy agency, activated explosive drones within Iran itself. Among the dead were three of Iran’s top military leaders: Mohammed Bagheri, head of the entire armed forces; Hossein Salami, head of the paramilitary Revolutionary Guard; and Amir Ali Hajizadeh, head of the Guard’s ballistic missile programme. Fereidoun Abbasi, former head of Iran’s Atomic Energy Organisation who dismissed the possibility of an assassination, was among the few nuclear scientists killed as well.

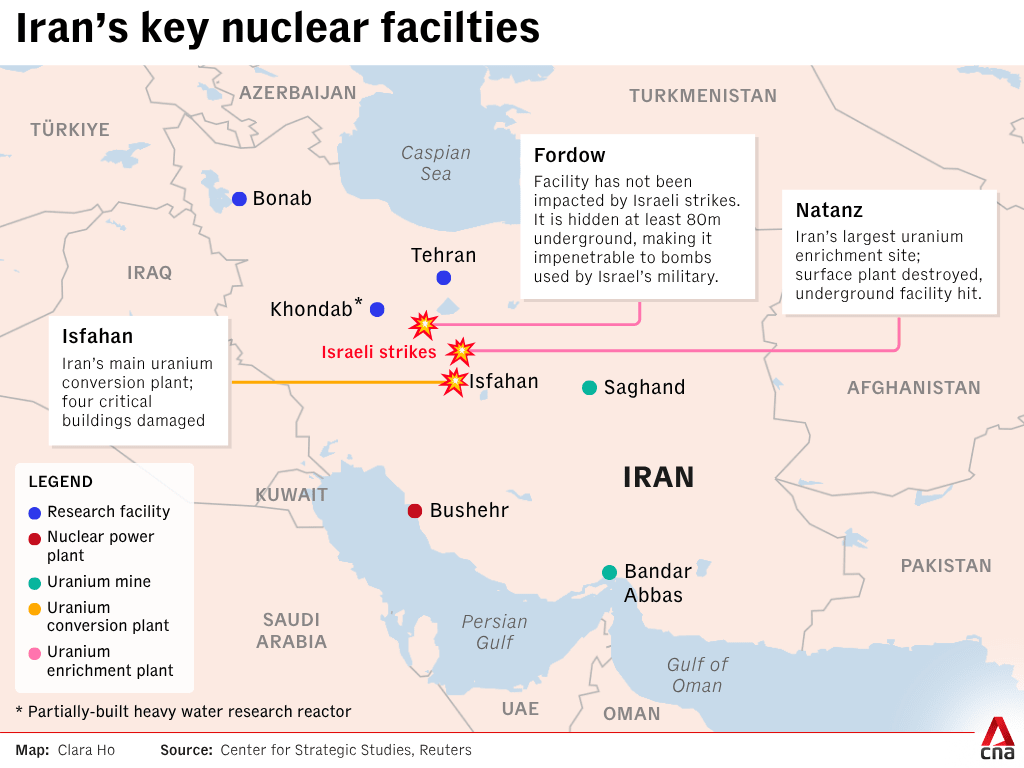

It is obvious that Israel is trying to cripple Iran’s nuclear goals. How does uranium get made into nuclear weapons anyway? First, uranium needs to be enriched in centrifuges by spinning uranium gas to increase the proportion of uranium-235 while removing uranium-238. These centrifuges, located at Natanz, were either severely damaged or completely destroyed on the first day of airstrikes. Next, the enriched uranium gas must be converted back into metal. Lastly, the nuclear core must be imploded using special explosives. Both steps will be severely hindered: Isfahan, which houses uranium conversion facilities and Parchin, which is a testing site for nuclear core implosions, were attacked.

The sore point for Israel, however, is Fordow. Fordow is hidden deep underground, impervious to any bomb that is available in Israel’s arsenal. The U.S., however might have a solution in the form of the GBU-57 MOP, a 13-ton bunker-busting bomb which is supposedly able to penetrate up to 60m of concrete. The latest intelligence Israeli dossier suggests that Iran had squirrelled away an unknown quantity of nuclear material that escaped the gaze of international nuclear watchdogs. Iran could continue refining fissile material in secret using a small number of centrifuges hidden deep in its Fordow base. If true, then the U.S. (read: Trump) might see fit to launch its own strikes against Iran.

What are Iran’s cards on the table?

The reason why I bring up Iran’s nuclear progress is that it plays directly into how Iran will react. Iran has a number of retaliatory measures at its disposal; the more desperate these measures, the worse it will be for the global oil market. Right now, Iran seems to be content with tit-for-tat. On June 13th, Iran responded with sustained waves of drones and missiles. By June 15th, both countries were trading strikes on energy and civilian infrastructure. Notably, Iran’s South Pars gas field — the world’s largest by far — as well as a number of refineries and oil depots in Tehran have been hit.

It is also important to consider Iran’s cultivated posse of foreign militant groups, dubbed the ‘Axis of Resistance’. This includes the Houthis in Yemen, Hezbollah in Lebanon, and Hamas in Gaza. Notably absent are the Hezbollah and Hamas, for good reason. Hezbollah is effectively decapitated with its leader, Nasrallah, assassinated last summer, and Hamas forces are decimated by 20 months of fighting against the IDF. Without strong proxies to act as Iran’s forward deterrent, Iran has less cards to threaten retaliation with.

And then there’s the continuity of Iran itself. The supreme leader, Ayatollah Ali Khamenei, and his Islamic regime is deeply disliked by young Iranians. On social media, some celebrated the killing of their generals, using barbecue emojis to mock their deaths. On June 13th, the death of Ali Hajizadeh, the air force commander, who had never expressed remorse for downing a passenger plane filled with Iranian students, was cheered online. On the ground, citizens are left to fend for themselves with no missile attack warnings and a lack of public bomb shelters. The fact that so many of Iran’s top commanders can be assassinated overnight so easily hints the extent of disloyalty Khamanei suffers among his ranks. A weak response might put the leadership in a position of weakness. On the other hand, an overtly aggressive retaliation (upping the nuclear ante, for instance), will risk enticing the U.S. in joining the fray, with much deadlier consequences.

Geopolitics has an interesting grey zone: the nuclear threshold. States like Iran, who operate just before this threshold, cannot negotiate from a position of strength. It is the reason why Iran has continuously sought to develop its nuclear programme since the 1980s; to race towards the protection that nuclear deterrence provides. Look at North Korea: Pyongyang’s nuclear success essentially made it immune from preventive strikes by its southern neighbour.

The theory of mutually assured destruction assumes that both actors operate under mutual vulnerability. But the fact that Iran is on the threshold of becoming a nuclear state throws these assumptions out the window. Iran cannot fully deter Israeli countermeasures because it lacks nuclear weapons of its own. But to do that, it risks suffering these exact countermeasures by Israel. This creates a “use it or lose it” dilemma: Israel faces a shrinking window to either disable, or delay Iranian nuclear progress, while Iran faces incentives to accelerate its programme to obtain inviolability status.

Shaking the oil barrel

The immediate economic consequence of the Israeli strikes was a jolt in the oil markets. On June 13th, the day of the strikes, the price of Brent crude jumped by 7% to over $74 per barrel, with intraday spikes reaching as high as 14%. This surge was not driven by any immediate, tangible loss of oil supply. Rather, it reflected a geopolitical risk premium, which accounts for the heighted possibility of an actual disruption. As of writing, the Brent price has inched higher to $76.

In October last year, this risk premium was worth around $5-10 when Hezbollah’s Nasrullah was assassinated and Iran launched about 200 ballistic missiles at Israel. Following this symbolic retaliation, oil prices simmered back down. A similar outcome this time would likely see the Brent fall back down to around the $68 area. Whether this conflict would de-escalate like before, however, is hard to say. Iran’s foreign minister Abbas Araghchi said that Iran is “not seeking negotiations with anyone” as long as Israel’s attacks continue. Netanyahu, meanwhile, stated that the battle will continue for “as many days as it takes”.

If status quo holds, and Iran continues its calibrated tit-for-tat missile strikes — which is increasingly unlikely as their missiles get continuously depleted — then oil prices will likely stabilise with a small risk premium. There are two exceptions, however, that will blow status quo out of the water.

The first is Iran attempting a partial or full blockade of the Strait of Hormuz, through which a fifth of global petroleum consumption passes through a day (or roughly 20 million barrels). This is rather unlikely, not least because the waterway is vital to Iran itself. If Iran really did block the strait, powerful nations would move very quickly to unblock the passage using their navies. On one hand, the U.S. wants oil prices to remain low. On the other, China is reliant on oil imports from Gulf states. The second exception, is Trump’s involvement. As of writing, Trump is still deciding on whether the U.S. should make a move on Iran. If it does, then how badly oil markets will respond depends exactly on what Trump does.

Assuming either the U.S. or Israel (or both) attack Iran’s oil wells. Iran is OPEC’s fourth-largest producer, exporting about 2 million barrels a day. Were Iran’s supply of crude oil to halt, oil prices might climb to $85-90 per barrel. But Iran’s Gulf neighbours have plenty of spare capacity; Saudi Arabia and the UAE alone have roughly 3 - 4 million barrels per day that they can bring online in a pinch. Suppose the worst-case scenario where Iran blockades the Strait of Hormuz. Saudi Arabia could divert exports through its East-West pipeline, which has a capacity of 5 million barrels a day. But the remainder of the Gulf states — Iraq, Kuwait and Qatar — have no other way to export, meaning Brent might hit $100 a barrel, according to Michael Haigh of Société Générale.

So what then? Historical precedence tells us that there is nothing much to worry about. Even during the “Tanker War” in the 1980s where Iran and Iraq saw over 200 oil tankers attacked in the Persian Gulf, the Strait of Hormuz was never closed, and oil prices stabilised quickly after an initial surge.

In all likelihood, status quo will prevail. The risk premium will evaporate as markets realise there is no actual threat to global oil supplies. Khamanei is both old and unpopular, and is likely to pass on the torch to his son, Mojtaba, who at times have been compared to Saudi Arabia’s Mohammed Bin Salman, a modernist. The Ayatollah’s decades-long struggle to nuclearize Iran protected by a ring of proxies has largely been a failure. His successor, Mojtaba or otherwise, might finally plot a less confrontational course that brings some stability to the region.

But for now, the world waits for the next big move; either by Iran, Israel, or the U.S.